In December 2008 I sat down to pay my bills and cried. I had dug a hole deeper than I could get out of. And every month it was getting worse and worse. I had to do something.

I was $15,000 in debt and took home about $800 every two weeks. I had rent, a car payment, a cell phone contract, DSL internet (but no cable t.v.), insurance and the occasional kid to feed. I am not a frivolous spender, but I had put everything from a mattress and box spring to gas to an MRI on my credit cards. I had nothing of substance to show for my purchases - no big screen t.v., no jewelry or designer clothes. My car could get from A to B and my knee could bare weight. I had hocked what I could - a couple of lenses, some scrapbooking supplies and a wedding ring that wasn't being used. I was down to the stuff that doesn't sell at garage sales.

I had heard Bob Brinker (a less annoying Suze Orman type who hosted a show called Money Talk) advise people in my position to go to Consumer Credit Counselling Service and talk to them about debt consolidation.

I instant messaged my manfriend and fessed up about how bad my financial situation had become. There were more tears. Angry ones. Embarrassed ones. Worried ones. SCARED ones. And all of them were fat and ugly. Lord, I am an ugly crier. I asked him if he'd come with me to the appointment I was mustering up the nerve to make. Yes, he said. I asked him if he'd stand by me when I was really poor. Yes, he said. I asked him if he thought I was stupid or weak. No, he said.

So I made the appointment.

I needed a second pair of ears to make sure everything I was told would come home with me. I needed a second brain to make sure all the questions got asked. And so on a cold, dreary day in January we entered the back door of an unassuming office building in Parma. We sat down with Casandra Hudak and I told her things about my money that no one wants to tell anyone. Hi. My name is Caroline. I don't make much money. I've spent more than I make, and now I'm in deep doo doo. Please help.

She looked at my income. She looked at my bills. She asked me how much I pay for haircuts and how often I buy shoes and why I didn't have a line item for clothing. She punched numbers into her calculator. She entered numbers into her spreadsheets. She clucked and shook her head and printed out the bad news.

It would take $435 a month for 42 months. All my credit would be shut off, CCCS would negotiate a lower interest rate, all over limit fees would be waived. Late fees wouldn't be an issue because on the 20th of every month CCCS would take their money and make the payments on my behalf, and, unlike me, they would be really kick ass about making payments on time. I had to agree not to apply for any credit cards for the duration of my time in the program and if their auto-deductions were declined more than once I would be kicked out of the program and left to the mercy of my creditors.

She pointed out that haircuts and clothing weren't going to be something I could afford. She advised me not to do the program because there simply wasn't enough income to make it happen without other issues cropping up. What if your car breaks down? What if I had a medical emergency that required copays?

Yeah? What if? Because I didn't have any money left over after making my payments anyway. So please, just print out the contract and give to me to sign before I lose my resolve.

We left and it was still cold and dreary, and I was still scared and embarrassed and worried, but I also had butterflies of giddiness. I could get out of this mess. There might be an end.

And for the last 41 months I've watched as CCCS has taken $435 out of my checking account. Most months I've really sweated that money being there. I've learned to time my other bills and my paychecks to accommodate that withdrawal.

The bills still came. Sometimes I would open them and throw them away in disgust. Progress was steady, but it was SLOW. Lower interest rates were helpful, but because there was interest, my monthly payments were making dings, not dents, in my total debt.

Most months I told myself that I was better off not looking at the bills. They got shredded in a sealed envelope.

Over the last three and a half years I've heard surprisingly little from CCCS. I got a letter letting me know they were being absorbed into Apprisen Financial Advocates. There was a tiny flurry of communication a year ago when my bank switched my debit card from Visa to MasterCard. Aside from that, we haven't been in touch. They make it surprisingly easy to hand over all your financial dirty laundry and let someone else deal with it while you walk away and try to not spend money.

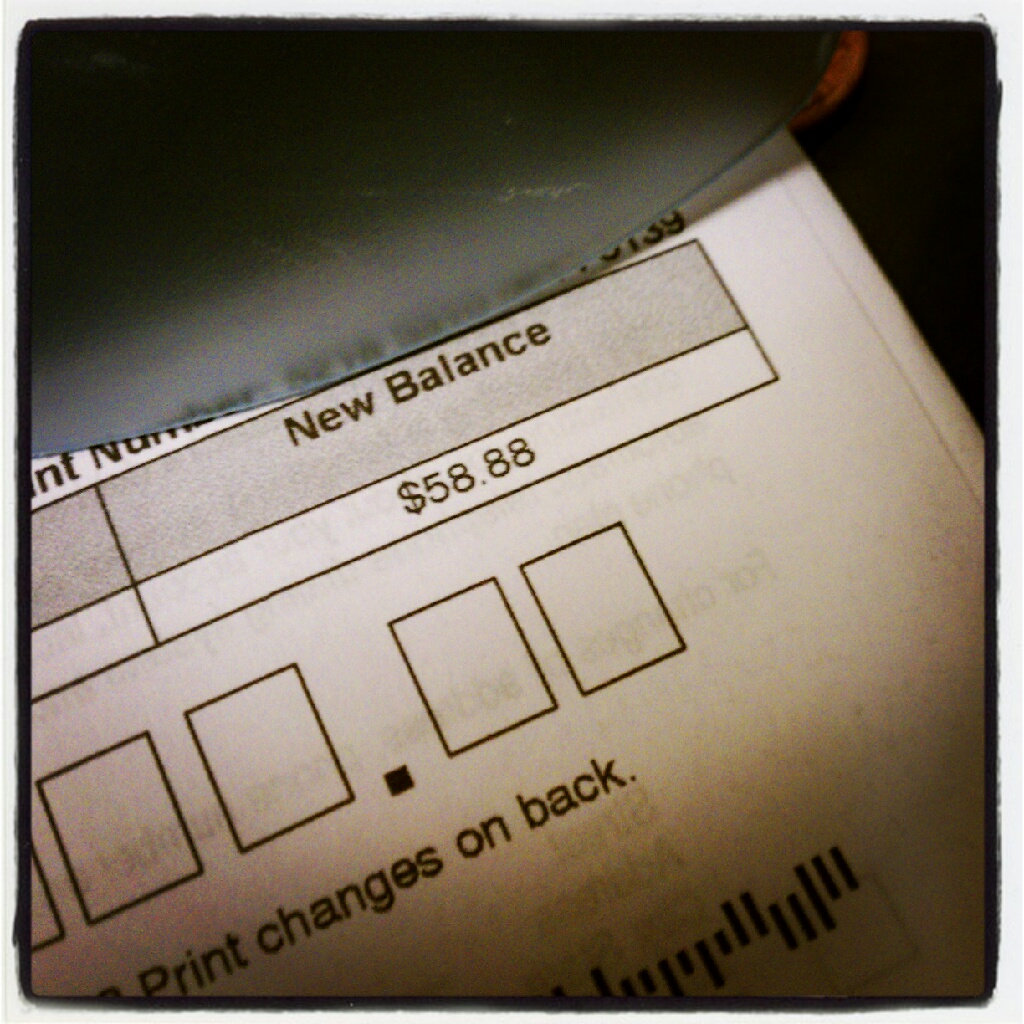

And for all that lack of communication, I was a little surprised to get a message today from Thomas at Apprisen, asking me to call him about my "services" with them. Once I placed the name I steeled myself for the worst: it was going to take longer than predicted or some other yuckiness. Megan answered and I told her I was returning a call from Thomas. Rather than passing me off, she took my name and social security number and proceeded to tell me that I had a zero balance.

What does that mean?

I am done. I have payed everyone off. A month earlier than planned. I dutifully took notes through the rest of the call, writing down when I should check my credit report (3 to 5 months), what I should look for there (anything that looks out of place), the website that they recommend (annualcreditreport.com) and why looking at the credit report is more beneficial than just buying your scores. I listened politely, asked her to verify that they had my correct address to send the final paperwork, thanked her and hung up.

And then I cried again.

First, let me just say how much I hate blogger: GAH! I hate blogger! I'd accuse it of being the least friendly user interface EVER, but that's just not true. Plus, it's flipping free, so I can't go exaggerating about it. But I do not like it, Sam I am!

First, let me just say how much I hate blogger: GAH! I hate blogger! I'd accuse it of being the least friendly user interface EVER, but that's just not true. Plus, it's flipping free, so I can't go exaggerating about it. But I do not like it, Sam I am!